As you have seen in the news lately things are changing in the UK not only to combat money leaving the UK but to also combat tax evasion. There is a misconception that tax avoidance is the same as Tax evasion, it’s not.

Definition of Tax Evasion

“Income tax fraud is the wilful attempt to evade tax law or defraud. Tax fraud occurs when a person or a company does any of the following: Intentionally fails to file a income tax return. Wilfully fails to pay taxes due. … Makes fraudulent or false claims”

Definition of Tax Efficiency

“Tax efficiency is an attempt to minimize tax liability when given many different financial decisions. … Other options to reduce tax liability include tax–efficient mutual funds, irrevocable trusts and tax-exempt commercial paper”

So, this is where things get interesting for all UK Expats as things get complicated, VERY COMPLICATED!

Take a look at the below Fact Sheet and have a think about what you will be doing, not now, but in a few years, will you go back to the UK to retire because of the NHS, because of family, most do believe it or not and then forget about everything, until it’s too late.

Legislation Changes

- Legislation changes impacting on UK Expats , Non-UK residents with residential property and future UK resident

Are you:

- Were born in the UK?

- Frequently visit the UK and have ties to the UK?

- Have residential property in the UK?

- Plan to live in the UK but not born there?

- Planned to return as a ‘Non Dom’?

UK Residency

As you live overseas and pay the jurisdictions taxes you live in you become a ‘tax resident’, this is not the same as ‘Resident’

We see this on many occasions and unfortunately people just DON’T know the correct way to calculate this

We hear;

I am not UK resident, I only spend the summer holidays there’ BUT,

- If more than 16 days you CAN be UK resident

*Must look at number of days and ties to the UK to determine residence and exposure to the tax system

Residency, the Basics

For a UK tax liability to arise;

- HMRC use: The ‘Theme of ‘connecting factors to UK’ which means that there:

- Must be a UK source for the Income/Capital Gain

or

- Person must be UK resident

Historic UK Residency

This can be used but only for guidance as this is historical and reasonably ambiguous and things change

IR20………

Then

HMRC6

UK Residence Developments

The developments were brought in 2013 and without much advertising so previously were you could go by the 90 day rule these have been brought in;

- Statutory Residence Test enables the tax payer to have more certainty since April 2013

- Test based on connecting factors

- Concept of ‘Ordinarily resident’ no longer used

Connecting factors – Residence

This has now become a 3 part test called ‘Connecting Factors’, where you are able to confirm/test your residency

- Part A contains rules which if met confirm that the individual is non-UK resident

- Part B has rules where if met a person would be considered to be UK resident

- If neither Part A nor Part B apply, Part C looks at ‘connecting factors’ for tax purposes – too many and person could remain UK resident

- Most UK expats will have ‘connecting factors’ to the UK, this is where planning is required

Statutory Residence Test 1

- Part A of the test will conclusively determine that an individual is not resident in the UK for a tax year if they fall under any of the following conditions, namely they:

- Were not resident in the UK in all of the previous three tax years and they are present in the UK for fewer than 45 days in the current tax year; or

- Were resident in the UK in one or more of the previous three tax years and they are present in the UK for fewer than 16 days in the current tax year; or

- Leave the UK to carry out full-time work abroad, provided they are present in the UK for fewer than 91 days in the tax year and no more than 31 days are spent working in the UK in the tax year

Statutory Residence Test 2

- If Part A of the test does not apply, an individual will be conclusively resident for the tax year under Part B if they meet any of the following conditions, namely they:

- Are present in the UK for 183 days or more in the current tax year; or

- Have only one home and that home is in the UK (or have two or more homes and all of these are in the UK); or

- Carry out full-time work in the UK

Statutory Residence Test 3

- Where neither Part A or Part B apply conclusively, then the factors of Part C are used as the

‘Tie Breaker’

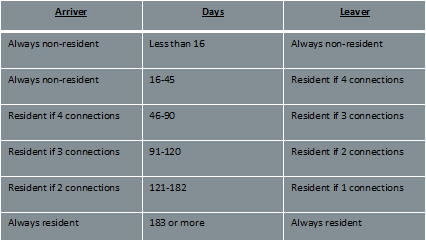

Tie breaker – Connecting Factors

– Family (defined as spouse, civil partner, common law partner and minor children) resident in the UK

– Available accommodation in the UK

– Working in the UK for 40 days or more days per tax year (working 3 or more hours a day constitutes a working day)

– Spending 91 days or more in the UK in either of the last two tax years

– Spending more time in the UK than any other single country

- Also depends on whether you are an ‘Arriver’ or a ‘Leaver’

Connecting Factors – How Many Are Required?

Case Study – Arriver

Mr D is a businessman with homes in various countries. He has not been resident in the UK prior to 2015-16. He has business interests in the UK and owns a house in London but, until 2015-16, he spends only a few days in the UK each year. In 2015-16 his wife moves to the UK to live in the London house with their two children. His wife and children become resident in the UK.

The children enrol in local schools and Mr D visits whenever he can. He spends 95 days in the UK in 2015, 45 of them working. He stays in the London house on days when he is in the UK.

Decision:

Mr D is resident in 2015-16 under Part C of the test. This is because he spends 91 days or more in the UK and has 3 connecting factors:

- A UK resident family;

- Accessible accommodation in the UK; and

- Substantive UK employment

Case Study – Leaver

Mrs E has been UK resident for several years, always spending more than 250 days per year in the UK. She has a successful IT company and now decides to create a new branch of the business in South Africa.

In 2015-16 she buys a house in Cape Town and spends a large amount of her time there. Until the new branch is established her family will remain resident in the UK and continue to live in the family home. She commutes back to the UK when she can, staying with her family when she does. She is in the UK for 93 days.

Decision:

In 2015-16 Mrs E is resident in the UK under Part C as she spends 90 days or more in the UK and has 3 connecting factors:

- A UK resident family; and

- Accessible accommodation in the UK; and

- Spent 91 days or more in the UK in the previous tax year.

Residence – Summary

- Plan to be challenged , keep evidence of arrival/departure

- Don’t simply rely upon ‘day counting’

- If claiming non-residence be aware of ‘everyday’ connections

- If you are UK resident, you are subject to tax on your worldwide income and gains

- Losing UK residence status is not as easy as you think, retaining it can be easier.

- HMRC is interested in everybody, not just ‘high profile’

- Care using UK as a ‘correspondence address’ OECD common reporting standards.

What is Domicile?

- Generally ; The country that the person treats as their permanent home, or lives in and has a substantial connection with

- You cannot be without a domicile

- You can only have one domicile at a time

- You are normally regarded as domiciled in the country where you have your permanent home.

- Your existing domicile will continue until you acquire a new one

UK Domicile

We hear ‘I don’t have a problem, I was born in the UK but I’m Non-Dom now’ so often when trying to assist UK Expats, so:

- Born in the UK = UK domicile of origin

- Can be lost, but difficult and open to challenge (Barlow Clowes v Henwood)

- If you move to another country , you revert back to your domicile of origin

- If retained on death, exposure to all UK taxes on worldwide assets

Your domicile is distinct from your nationality, citizenship and your residence status, although these can have an impact on your domicile

UK Domicile/IHT Rules

General

- Nil rate band of £325,000 each

- Transfers on death between UK Dom Exempt from IHT

- UK Dom/Non-Dom , only up to £325,000 (after NRB)

- Election can be made to be UK Dom following death of UK Dom spouse but…. 2 year limit and residence requirement

- Although all assets free of IHT following election, will remain UK Dom for next 4 years, even if UK Domicile renounced and leave the UK.

- 15/20 rule for deemed domicile

Legislation Updates – UK Domicile Rules

Retrospective from April 2017

- If born in the UK & return to UK = immediate return to UK Dom

- If born in the UK, retain UK Dom for 4 years after leaving

- If acquiring UK domicile of choice, election remains for 4 years

- ‘Lifelong’ non-domicile status to end

- New 15/20 Deemed Dom Rule

- UK property held through Offshore Company looked through

- Remittance basis cannot be claimed once UK Dom

- Asset value can be rebased to April 2017 value

- Domicile ruling is in respect of all taxes, not just IHT.

Inheritance Tax & Domicile

- 40% tax charge on value of estate above £325,000

- Gifts between UK Dom spouses /civil partners exempt

- Care required where Non-Dom spouse / civil partner

Individuals with a UK domicile of origin who planned to return to the UK as a Non-Dom must review their planning

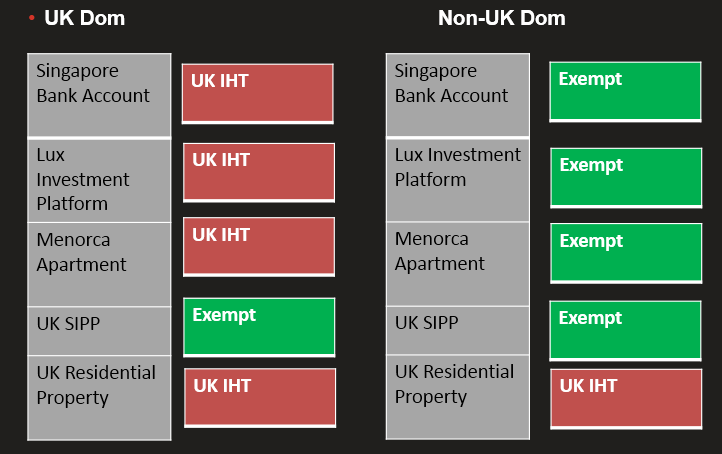

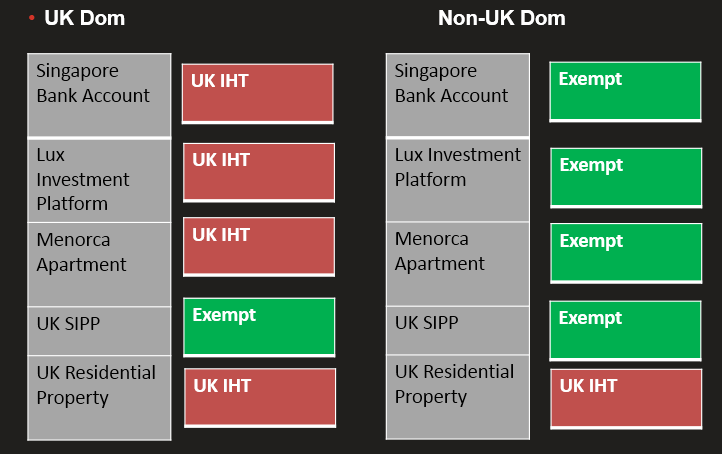

Inheritance tax & Domicile

John has lived outside of the UK for the last 15 years working as an IT contractor and has the following assets in his estate:

Singapore Bank Account £250,000

Luxembourg Investment Platform £150,000

Apartment in Menorca £175,000

UK SIPP £100,000

UK residential property £200,000

What is his UK IHT Exposure if he returns?

Do You Have Residential Property in the UK?

- IHT Irrespective of domicile/residence status

- Ownership through a Company no longer provides protection

- How will HMRC know?

- Checks will be made when property is to be transferred as to whether property has ever been included in IHT valuation

- Options – Insure against Liability sell or change to PPR?

- If selling, was valuation obtained April 2015 for CGT?

UK Residential Property

- ATED provisions in place since 2013 for HVRP that is ‘Enveloped’

- ATED allowed charge to be paid to continue to avoid SDLT & IHT

- IHT protection lost on all UKRP irrespective of value

- IHT liability is the value of the ‘structure’ that relates to the UKRP

- Debts can be offset against the value but loans between connected parties can not

- Is there any point in paying this charge if no IHT benefits?

IHT and the Family Home

This is another we hear a lot ‘We don’t need any planning, we have a £1m IHT allowance’, wrong !

Restrictions

- If you do not own a residential property, there is no £1m threshold!

- There will be a tapered withdrawal of the additional nil-rate band for Estates (not the property)

- With a net value of more than £2 million. This will be at a withdrawal rate of £1 for every £2 over this threshold.

More Restrictions….

- It will not apply to reduce the tax payable on lifetime transfers that are chargeable as a result of death (UK Dom to Non Dom)

- A property which was never a residence of the deceased, such as a buy-to-let property, will not qualify.

- If property value is less than allowance, balance can’t be used to offset IHT on other assets

Even More Restrictions….

- A person who dies with no direct descendants will not be able to benefit

- Not restricted to UK properties only however, the property must be within the scope of UK IHT and included in the deceased’s estate.

- Cannot be claimed by Non-UK Doms unless the home is in the UK

Non-Dom Planning

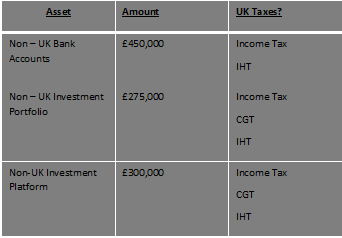

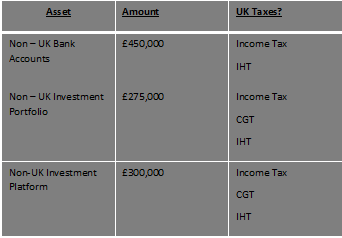

- Jane is John’s wife, she also works in IT and will be moving back to the UK with him. She was not born in the UK however, it’s highly likely they she will be deemed domicile in the future. She is concerned that the wealth that has been accumulated is going to be eroded by the UK tax system. She requires access to her capital and isn’t keen on paying the remittance basis charge.

She has the following assets:

- Non UK Bank accounts £450,000

- Non UK Stock Portfolio £275,000

- Non UK Investment Platform £300,000

UK Tax Exposure?

What is the remittance basis tax charge?

Annual tax charge to prevent non-UK source income and gains from being taxed. Only applies to Non-Doms.

First 7 years £0

7 / 9 Years £30,000

12 / 14 Years £60,000

17 / 20 Years £90,000

Under new legislation more than 15 Years all assets will taxable as deemed UK domicile

Non-Dom – Moving to the UK

This is what you will have to pay:

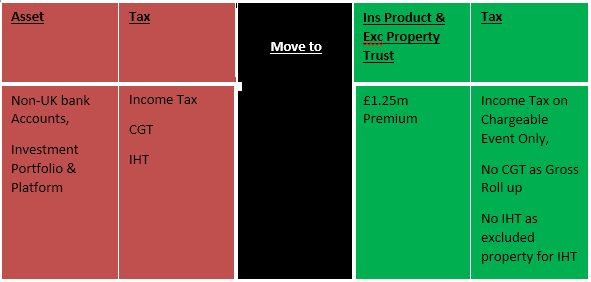

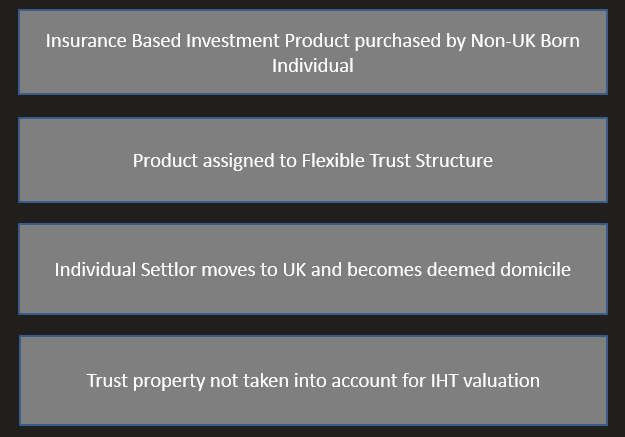

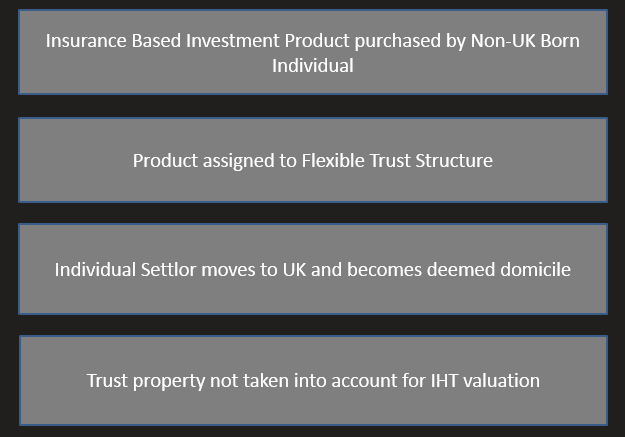

By Using Isle Of Man Insurance Product and Trusts

Excluded Property Trust

Planning Objective

- IHT mitigation , access to trust fund

- Generally used by those who:

- Are currently non-UK domiciled but who may become UK domiciled in the future

- Want to ensure that post April 2017 rules do not impact planning

- How does it work?

- Assignment of Non-UK situs property (IOM Insurance Product) to trust

- Person who creates trusts has unrestricted access

- As trust fund created prior to UK Dom, not taken into account for IHT

IHT Planning – Excluded Property Trusts

UK Tax Treatment on Creation

- N/A , on creation as Settlor is not UK domiciled therefore, property is ‘excluded’ from IHT

- Where Insurance product used, CGT protection and IT deferral

Restrictions

- Must be certain of domicile status

- Must only contain non-UK situs assets

UK -Dom Planning Post April 2017

What can John do?

- He returns to his UK domicile of origin as soon as the residency test met

- Cannot claim the remittance basis of taxation

- His corporate structures holding properties are looked through for IHT

- All non UK source income & gains are taxable in the UK

- Worldwide estate is subject to IHT

Popular Planning using Tax Efficient Investment

Accepted non-offensive IHT Planning?

- Mostly Trust based Insurance Co’s investment products that facilitate

– IHT mitigation through Outright Gifts

– IHT effective Loans/Asset Freezing

– Immediately Discounted Gifts

Importantly, these structures ARE recognised by HMRC as legitimate tax planning and are not caught by any Anti-Avoidance legislation

We cannot stress enough that the correct Estate Planning, Tax Planning, Succession Planning, call it what you will is vitally important and does not have to cost as much as you think, we can look at your current situation and gauge the best way forward, don’t leave it and think it’s OK. Also using UK based advisers or lawyers can also not work too well, give us 15-20 minutes of your time and let us plan your future correctly with no obligation.

Have a good day

All the best

Stuart

CEO

Farringdon Group

+60 3 2026 0286