Courtesy of BBC News

I thought I would share this information with you as it is quite significant numbers and HMRC will definitely be looking at this with a fine tooth comb, potentially making new legislation or even imposing more taxation implications, let’s see.

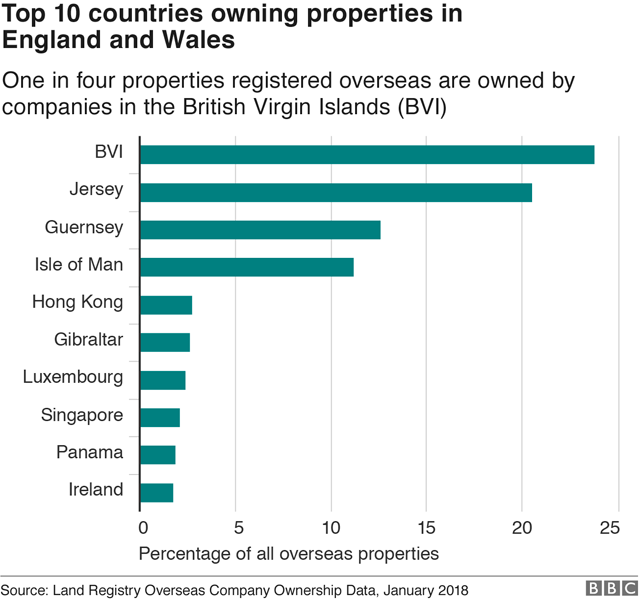

A quarter of property in England and Wales owned by overseas firms is held by entities registered in the British Virgin Islands, BBC analysis has found.

The Caribbean archipelago is the official home of companies that own 23,000 properties – more than any other country.

They are owned by 11,700 firms registered in the overseas territory.

The finding emerged from BBC analysis conducted of Land Registry data on overseas property ownership.

The research found there are around 97,000 properties in England and Wales held by overseas firms, as of January 2018.

It adds to concerns that companies registered in British-controlled tax havens have been used to avoid tax.

Close behind the British Virgin Islands (BVI), which has a population of just 30,600, are Jersey, Guernsey and the Isle of Man.

Of the properties owned by overseas companies in England and Wales, two thirds are registered to firms in the British Virgin Islands, Jersey, Guernsey and the Isle of Man.

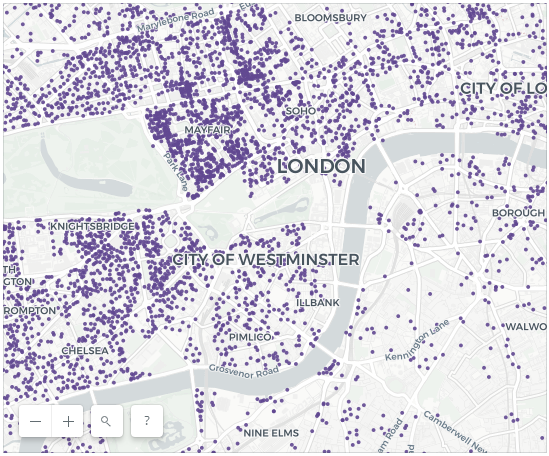

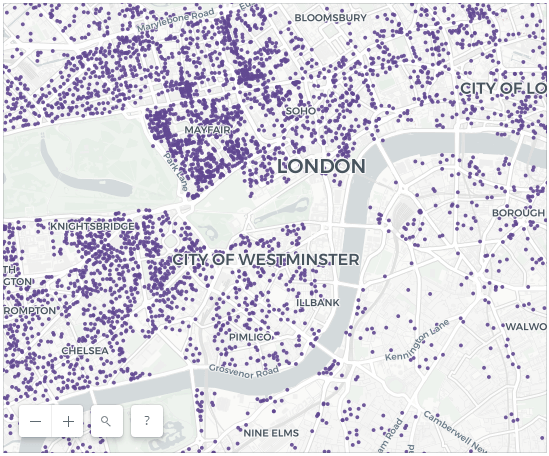

Where are the properties owned by overseas companies located?

Click or tap on the properties owned by companies registered abroad to find out more

Map built by Carto. If you can’t see the map, please click here to open the same story on the BBC News website.

Note: Property locations are approximate based on the centre point of the postcode they fall into. As such they have been removed when the map is zoomed to the most detailed levels. Ownership information like the company name and country refer to the ultimate owner of the property, not necessarily the person or company that may rent or occupy the property.

Many foreign UK property owners are also officially headquartered in Hong Kong, Panama and Ireland.

The analysis provides a new picture of ownership of property by overseas companies in England and Wales following a decision last November to make the database public and free to access.

It found:

- Close to half (44%) of all properties owned by overseas companies in England and Wales are located in London

- More than one in ten (11,500) properties owned by overseas companies in England and Wales are located in the City of Westminster

- More than 6,000 properties owned by foreign companies are in the London borough of Kensington and Chelsea.

The government of the British Virgin Islands said it was incorrect to label the country as a tax haven.

It said that there were many practical reasons why UK properties might be owned by companies incorporated in the BVI.

It argued that BVI companies can bring together multiple investors and owners, which is useful for big commercial property deals that have investors in more than one country.

The BVI also said that it shared “necessary information” including ownership details with relevant authorities.

Among those entries in the database that disclosed a price, the most expensive was the former headquarters of the Metropolitan Police, New Scotland Yard, at 8-10 Broadway.

The site was purchased by the Abu Dhabi Financial Group in 2014 for £370m from the Mayor of London’s office. But it is officially owned by a Jersey-based company called BL Development.

The 1967 multi-storey block has now been demolished to make way for “a luxury collection of one to five bedroom apartments across six architecturally striking towers”. These range in price from £1.5m to more than £10m.

The leasehold of Admiralty Arch, the former government building off Trafalgar Squarer that straddles one end of The Mall, was sold to hotel developer Prime Investments for £141m. It is registered to a Guernsey-based entity, Admiralty Arch Hotels Ltd.

While the most expensive buildings are commercial properties such as hotels and office blocks in prime central London locations, many are residential properties rather than business premises.

Take Green Street, London W1 – a residential street of highly-desirable four-storey redbrick Victorian terraces, fronted by smart wrought-iron railings.

Walking east to west you’ll pass one terraced residence owned, according to the latest records, from the Turks and Caicos Islands by a company called Alliance Property Ltd. Next door is another residence owned by Lily Holding & Finance Inc, registered in BVI.

In all, 15 properties on the street are owned by companies registered in the British Virgin Islands, four in Jersey and one in the Isle of Man. Others have owners in Italy, Hong Kong and Singapore.

Accountants used to recommend using an offshore company to overseas buyers of property in the UK as a means of avoiding inheritance tax when the owner passed away.

“Until April 2017, if you weren’t resident in the UK and held a residential property via a company it was not counted as being an asset for UK-based inheritance tax purposes. So having a property through an offshore company meant you escaped inheritance tax,” says Mark Giddens, of accountants and consultants UHY Hacker Young.

However, since last year the government announced plans to close the loophole, dramatically reducing the attractions of offshore ownership of residential property.

Offshore jurisdictions such as BVI still offer buyers who wish to keep their names out of the public realm greater privacy than they would enjoy if they purchased their property as an individual.

While most tax havens have agreed to take part in automatic information exchange, allowing law enforcement agencies to discover the individuals who enjoy beneficial ownership of an offshore company, their names will not appear in the published data.

In contrast to residential properties owned by individuals, the Land Registry does not always release “price paid” figures for properties owned by companies.

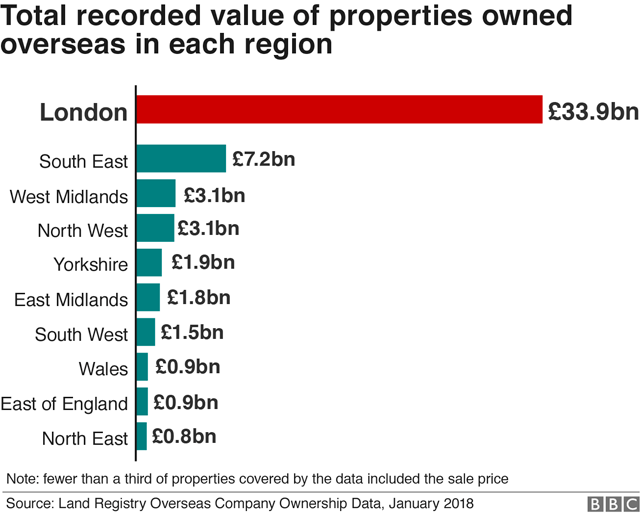

Adding up the 27,835 properties whose most recent sale prices we know, the price paid was just over £55 billion.

Notes: The BBC analysed the January 2018 Overseas Companies Ownership data made public by the HM Land Registry. The data is accurate up to January 2018 and contains around 97,000 title records of freehold and leasehold property in England and Wales, registered to companies incorporated outside the UK. The map shows 71,000 of the 97,000 addresses. Those missing had incomplete data.

All the best & have a good day

Stuart

CEO

Farringdon Group

+60 3 2026 0286