The independent asset manager, which oversees about $1bn in high-net-worth investments in Asia, has joined forces with the Baker Tilly JFC Group to collaborate on infrastructure financing.

The duo will specifically focus on debt advisory and syndication including long-term funding via a structured finance route known as the BETA International Funding Program.

The program is designed to help both private companies and governments finance infrastructure projects that are greater than $500m.‘We see Baker Tilly’s BETA International Funding Program as being a big part of that across Asia and we are very pleased to assist them with this endeavour,’ said Farringdon Group CEO Stuart Yeomans.

‘With the global recession caused by the pandemic now beginning to bite, it is more important now than ever, that governments and corporates look to the future and begin work on long delayed projects, that can help turn the economy around,’ he said.

In Dubai, Farringdon holds a Category 3C fund management license issued by the Dubai Financial Services Authority.

The firm is on the lookout for partnerships to grow its business in the Middle East.

Its Asia operations work with a range of private banks and custody platforms to offer clients solutions covering investments, banking, tax and succession planning needs.

Mago JB Singh Founder – Principal & Group Managing Partner Baker Tilly Middle East had this to say

We are delighted to be collaborating with a company as energetic as Farringdon Asset Management in the most important and critical area of Project Finance which is the immediate need for all economies more particularly developing economies. Given our experience of 45 years in Project Financing, Project Management, Industrial & Manufacturing Consulting, we hope that our two companies can go on to work together and assist companies and corporates on their projects in the future that can mutually benefit both companies’ clients.

Following the opening of a wealth business in Singapore

The Dubai Financial Services Authority (DFSA) has granted a category 3C fund management licence to Farringdon Asset Management, International Adviser can reveal.

Farringdon’s branch office will be based in the Dubai International Financial Centre (DIFC) and is headed up by Stuart Yeomans, who was formerly chief executive of Farringdon Group in Malaysia.

Having spoken with relationship managers on the ground, Yeomans said: “The common consensus was that the DIFC was the place to set up for quality and regulation.

“Our aim is to build a small but effective team within Dubai and focus on quality rather than quantity. We have managed to build a solid foundation in the south-east Asia region and the Middle East is next.”

Moving forward, he will speak to private bankers and financial consultants throughout the region and “look to bring the right candidates into our growing company”.

“One major factor that sets us apart is that we will be one of the only players in town offering full partnership within the firm for the right people. I feel that when a business revolves around one person at the top there is too much focus on building their wealth, as opposed to the end client.

“Our model is focused on the right reliable close-knit team that performs for their colleagues and clients,” added Yeomans, who was named in International Adviser‘s IA 100.

Taking a stringent approach

Farringdon Group is looking to replicate the success it has experienced in Singapore and south-east Asia, said Martin Young, chief executive of Farringdon Asset Management.

“The DIFC and Dubai are increasingly seen as one of the world’s major financial hubs and we believe, given our expertise in the high net worth and ultra-high net worth space, we can offer a unique service level to clients in the Gulf Cooperation Council and Middle East and North Africa region.

“The regulatory regime offered by DFSA is second-to-none in its stringent approach and we believe that both clients and staff will increasingly look to have their assets managed by DFSA-regulated firms.

“These needs will grow exponentially as insurance brokers and consultants are gradually removed from their ability to advise on and manage assets under the increased burden of regulations,” Young added.

Farringdon Asset Management would like to thank Kirsten Hastings, editor of international adviser for joining us at our 1 billion dollar party and for this article.

Over the past 11 years, we have amassed a client bank of well over USD1 billion across our offices and with a recent addition of Dubai, we are now proud to announce our new set up in Labuan.

Labuan FSA announced at the beginning of 2019 that all companies registered in Labuan, will need to maintain an office and staff in Labuan or face changes to the way they are taxed and monitored.

Stuart Yeomans Now CEO of Farringdon Asset Management (Dubai) stated that “Although we are moving and setting up a physical operation in Labuan, we will still maintain our offices in Kuala Lumpur. We have made some changes to the office and are happy to announce Daniel Carnie will replace me as the new CEO of Farringdon Asset Management (Malaysia: Formally – Farringdon Group)

Daniel has been working under myself for over 8 years and is 100% ready to make the big step into becoming the new CEO and to run his new office. There is no end to changes to our industry and even this week we have been informed by clients that competitors are saying we are closing our door. It just goes to show that no matter what you do; like expand into Singapore and Dubai, then into Labuan, not to mention break the USD1 billion barrier, there is always a way in which our industry twists things. These types of rumours are exactly why we need someone knowledgeable at the top and Daniel is the right man for the job.

Daniel commented that “It makes us glad that we made the move to asset management and have expanded the team significantly to ensure that client assets are managed correctly.

Our main aim now is to focus on managing current clients and we are not focused on dozens of sales people; we are now strongly working from referrals and introducers and no longer need to focus on a core sales team. This is good news for prospects as we see the curtain coming down for these heavily sales driven teams as opposed to selecting the lowest cost investments that perform and working from referrals.

The office has gone under some recent restructuring to ensure that in the long term it is viable; we have new introducers that pass us business that they can’t do anymore, and we are always on the look out for good quality consultants. We are specifically after people with USD10 million in AUM to join and we have the correct set up to ensure that they are looked after correctly.

New members of our team will have an existing book that our asset management team can assist on lowering fees for the end client, whilst getting them better performance. This really is possible with our knowledge and because we control a relatively large AUM we can get better deals than most companies.

Stuart closed by saying that people will be surprised that very soon, we are on target to exceed US$2 billion under management this year which will make us one of the dominant players in the offshore wealth space in the world.

The past year has officially been the worst year for investments since 2008 and it was capped off by the worst December since 1931. Despite strong economic and job performance from most major economies, markets have been thrown off balance by the actions of Donald Trump and his interactions with the US Federal Reserve as well as his ongoing trade battles with China and now his shutting down of the US Federal Government. However, as we enter 2019, there is cause for optimism and markets have already begun to rise substantially in the first week of 2019.

The Federal Reserve

Donald Trump brought in Jerome Powell to replace Janet Yellen at the Federal Reserve. Trump’s original intention was that Powell would go easier on interest rate rises than Yellen had previously done. However, almost as soon as he took over at Fed, Powell began to raise rates sharply and unwind the long-standing QE assets held by the Federal Reserve at a rate of $50 billion per month. Donald Trump has responded by describing the Federal Reserve as one of Americas biggest enemies. This spat culminated in the Federal Reserve once again raising rates in December against all expectations of the market, which is the principal reason for the sell off in assets at the end of the year and the reason for equities experiencing their worst December in 87 years.

Quickly realizing the folly they have created, Jerome Powell came out on the 4thof January and issued a statement stating that the Federal Reserve will respond flexibly to market conditions and may consider halting the unwinding of QE. The Fed did much the same in 2013 and 2016 following the so-called Taper Tantrum. This has been the principal reason behind the rally of early January.

Oil Prices

Oil Prices were sent significantly lower in the last quarter, again by the actions of the Trump administration. In expectation of harsh sanctions to be imposed on Iran, key producers in Saudi Arabia and Russia had substantially increased production to make up the short fall in global crude supplies once Iranian production was removed. In the traditional Trump style at the very last minute almost all countries that purchase crude from Iran were awarded exemptions from sanctions by the US to continue doing so. This left a massive over supply in the market. It is unlikely that the Saudis and Russians will be fooled again and will likely refuse production increases next time Trump threatens sanctions on Iran.

China

2018 saw US equities loose as much as 10% at the start of Trump’s Trade war with China. While US Equites recovered in the middle of the year they have fallen again. Much of this fall has been led by Tech companies such as Apple who have seen production costs rise and have also experienced drops in sales in China. Chinese equities have dropped by as much as 40% in 2018 in Foreign Currency Terms. Trump and Xi Jinping have now met in Argentina and had what were described as very productive talks. The Chinese are already making trade concessions but it’s open to debate if this is enough to change Trump’s policy on Tariffs.

US Government Shutdown

The Republican Congress refused to approve $5 billion in funding for the Trump wall with Mexico. The New Democratic Congress is also continuing to hold to the same position. This has led to a shutdown once again in the US Federal Government with 25% of Federal staff going unpaid. While this in itself is insufficient to send markets into a downward spiral it all added to the negative sentiment at the end of the fourth quarter.

Moving Forward 2019

The drops in markets across the fourth quarter have to a certain extent removed much of the risk of an inflationary bust in the world economy that may have happened in late 2019 or early 2020. Central banks are likely to pull back on interest rate rises and countries like China look set to begin full-on stimulus again. The first quarter of 2019 will remain volatile, however there is now substantial room for growth in investments this year. Historically, bad years are always followed by good years in the stock market and many markets from China’s Shang Hai composite to the UK’s FTSE 100 are at their cheapest valuations in years.

The Banking industry is ever changing and versatile. Banks are constantly looking to adapt to the pressures they face, and one way to do so, is by adding or removing aspects of their international operations. Canadian offshore assets have increased by 38% in the last 10 years and there’s now over $1trn offshore in Chinese banks. Japanese and Indian banks have also seen an increase in their international operations. Meanwhile American and European banks are retrenching. There a number of positives and negatives when it comes to international expansion, below is a brief synopsis of some of the main points.

Why banks expand globally?

Client retention

Client retention is one of the biggest reasons for international expansion. Naturally, banks with a strong and positive reputation are more likely to retain and attract new customers. Finding solutions to existing client needs, even if that means navigating difficult regulation changes and operating in new areas, is an excellent way to build that kind of reputation. Operating internationally provides banks with further opportunities for investing in differing markets.

Economies of scale

International expansion maximises production of procurement, systems, operations, research, and marketing and minimises the costs involved.

Geographic diversification

Unsurprisingly, international expansion mitigates against geographical market fluctuations, through geographic diversification. This puts the bank in a stronger position as it is part of several markets. Therefore, it is less likely to be negatively impacted by a single market downturn.

Difficulties with international expansion

Additional costs associated with country risk

Unexpected changes in the host country’s environment can result in additional costs for foreign firms. Anything from economic growth to national debt, inflation to exports can affect country risk and cause banks to make changes accordingly.

Differences in culture, language and economic development

Larger banks often find it easier to expand into new places, as international expansion is often complex and can be costly due to differences in culture, languages and economic development. These differences can reduce efficiency and present challenges, such as dealing with regulations and the sharing of information.

Political instability and risk

Political Risk is the exposure to the effects of foreign governments’ actions on the value of investment in the foreign country. Therefore, before expanding their operations internationally, banks need to have a clear picture of the political environment of a country. Political instability can discourage banks from staying in a country, as demonstrated by CaixaBank (see figure 1), following the Catalan referendum. Due to the economic uncertainty, resulting from the referendum, the bank’s share price dropped and caused them to relocate to Valencia.

Figure 1

In short, changes in the global presence of banks are fuelled by a focus on the earning power of each country. Generally, banks should engage in international expansion, as it will allow them to reach a wider audience for their services, minimise transition costs, as well as diversify the sources of income. However, geographical expansion is more of a double- edged sword than previously thought, as banks will face additional operating costs, as well as face risks of political instability. Nonetheless, banks can still offset these potential risks by carefully choosing an adequate environment, which is not prone to political tensions (unlike the UK, which is still in the process of finalising its withdrawal from the EU).

One of the major difficulties that small businesses and new start-ups face is obtaining funding. In our contemporary society and with the use of technology, new firms have access to a plethora of fund sources. These include using the Internet for crowd-funding or even peer-to-peer lending. However, these sources are often uncertain as the firms do not know how much funding they will get with these methods. This means, that those start-ups often find themselves having to find funding from venture capitalists. The venture capital market plays a significant role in providing capital to a wide variety of enterprises.Although there are multiple benefits, new business owners need to be aware of the risks they are taking when engaging with venture capital firms.

So why accept the funding?

The first benefit of securing funding from a Venture Capitalist is that the business owner is not taking a loan. Therefore, the costs of operation will not include interest payments.

Apart from the financial safety, engaging with a venture capital firm may bring additional benefits. Inexperienced entrepreneurs stand to gain a great deal from venture capitalists’ wealth of start-up experience; they can gain insights on what to expect at various stages, what to worry about and what not to, and on how they are progressing.Tapping into this expertise can prove to be tremendously valuable in terms of business decisions or even human resource management, as the VC will help with the recruitment of top talents to maximize the productivity of the business. Being able to make better and informed decisions in these key areas, will be crucial for the growth of the firm. Moreover, if the owners have little experience in running a business and lack the knowledge to make informed decisions, the investors, holding a significant share of the equity, will be able to step in and have a say in how the business should run. This can be extremely valuable considering venture capitalists have extensive knowledge and experience in starting a business and how best to expand.

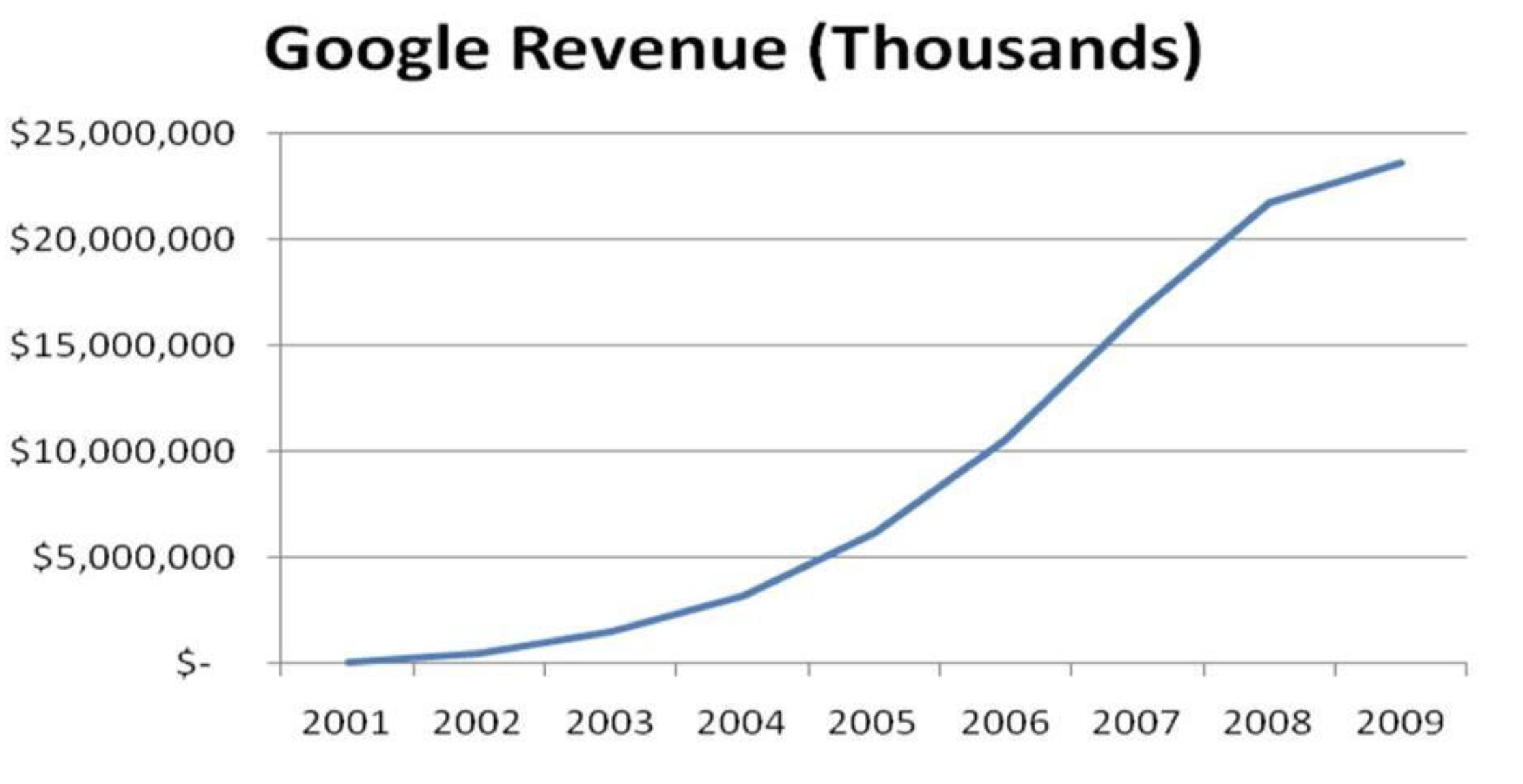

Figure 1 – Google Revenue

One striking example of a small projectbacked by venture capital firms to becomea global success is Google. It started as a project from two doctoral students who later gained backing by Venture Capitalist firm Sequoia Capital and Kleiner, Perkins,Caufield and Byers (KPCB).The business received $25 million, as the investors were confident about the potential growth of thebusiness, at a time when the Internet wasbooming. In 2001, on Sequoia Capital’s advice, Google founders hired the company’s first CEO, Eric Schmidt who remained the head of the firm until 2010. During this decade, we can see how much Google grew in terms ofrevenue (as seen in figure 1,) starting at nearly $70 million in 2001, to almost $25 billion in 2010.

But should small businesses be wary?

Of course! As a small business, turning to venture capital firms for a source of funding can prove to be a double-edged sword. So when opting for venture capital funds, instead of paying back as a loan repayment scheme, owners of the business will have to give up a significant part of their equity. According to Hellman (1998), this process will then allow “venture capital firms to hold effective control over the board, typically through a voting majority, and sometimes through explicit contractual agreements”.This means that the investors will effectively be significant shareholders of the company, subsequently, profits will also have to be distributed accordingly.

Due to this, the investors then become shareholders in the company. The size of their investment could determine how much influence they have on company decisions.

For example, if the investors have 20% to 50% of the shares, they have significant influence over the decisions, which means they can voice their opinion and influence decisions. However, if they have more than 50% of the shares, then the owners of the business lose management control, which means they often assume more direct control by changing management and are sometimes willing to take over day-to-day operations themselves.Although this is to guarantee the company’s headway, it can generate serious internal problems between the owners and the investors’ team. A telling statistic is that after 4/5 years from investment, more than half of the founder CEO’s are replaced!

Company owners who have been oustedfrom their own businesses include Steve Jobs with Apple, and Sandy Lerner, co-founder of Cisco. Lerner is no longer part of the company after losing control to a management group led by its early investor, Sequoia Capital’s Don Valentine.Cisco’s CEO, John Morgridge saw Lerner as the weak link of the firm, and it became clear that they shared different aspirations for the company. Subsequently, the board of directors decided to side with the CEO and let go of the founders.

So should you accept the investment in your business?

From a small firm, looking to get capital from venture capitalists point of view, having recourse to such funds will be beneficial for the business. Not only will the investors provide adequate financing, but also the support needed to help grow the business, by seeking new talents to perform the jobs, as well as give invaluable advice to better manage the business, which was the case for the current world-leading tech company, Google.

However, you also have to keep in mind that in order to access all these services, your control over the operations will be diluted because the investors will also have stakes in the business, via a percentage of the shares, which in turn, means that you partially lose ownership of the company. However, it is possible to mitigate against these setbacks, primarily through an agreement on the terms and conditions, prior to starting the funding of the business.

So, the short answer is yes! Accept funding, grow your company, but be careful that you’ll still be the person in charge, making the decisions!