What exactly is QE?

Economic growth has been correlated to both volume and velocity of money. When banks reduce their borrowing and lending to each other (as they did in 2009 due to high interbank interest rates) and when individuals rather save than spend, the flow of capital dries up and the economy contracts. The solution to stop this is to increase liquidity.

However, to get the financial system moving again it is not as simple. Central banks cannot simply force society to borrow and spend money. Therefore, to stimulate the economy, the monetary policy committee voted to reduce the Bank of England’s interest rates after the financial crisis. Subsequently, through open market operations, interbank, corporate and personal loans became cheaper. The basic principle is to flood the market with extra liquidity and encourage borrowing and spending with the new and cheap money. However, banks act cautiously and utilise this ‘cheap money’, to invest in safe government bonds that pay around 2% or invest it on higher risk assets and do not lend it out to firms and individuals as they are seen to be too risky. Therefore, this initiative does not create economy wide liquidity.

The second arsenal that the Bank of England can use to stimulate growth is to buy assets, consequently increasing the size of their balance sheet. They particularly purchase long maturity government bonds in the open market with newly created digital money. Through purchasing large amounts of bonds and affecting convexity, the prices rise and yields drop. With reduced yields, bonds become less desirable for banks and push them to invest in riskier sectors such as stocks, corporate borrowing and real assets. Subsequently, borrowing costs correlated with long-term interest rates such as mortgages/corporate borrowing rates declined, incentivising individuals and corporate borrowers to pull forward future expenditure.

This process of trying to stimulate growth is called Quantitative easing, however the bank of England cannot constantly undertake this as it needs the country to make money.

So what happens when Quantitative easing is phased out?

Advantages

The UK economic recovery has been steadily expanding for over eight years, more than the average business cycle. Inflation is now significantly above the 2% target, unemployment rate is below 4.3% (the lowest for more than 40 years) and consumer borrowing has been rising at double-digit rates. However, the state of the UK economy is on a tender balance, demonstrated by the fact that the BoE talked about raising rates on a number of occasions, though not acting on their comments. The pressures arise from greater economic uncertainty against inflationary pressures consequential from a weaker pound raising the cost of imports. However, the BoE did state that it would not sell down its £435bn stock of assets until interest rates increased to around 2%. They are currently at 0.5%. Clearly, Quantitative Easing has helped restore the UKs economy, phasing out Quantitative Easing now will help the economy to go back towards the norm of pre-crisis levels, in order to have enough reserves to tackle the next crisis. These reserves are necessary so that quantitative easing can be used again in the future.

Furthermore, through keeping such an unconventional policy in place for a long time has led to distortion in the markets. Deutsche Bank chief John Cryan favoured tightening of monetary policy stating that the time of ‘cheap money’ needed to end as it causes price bubbles and volatility.

Withdrawing QE would entice institutional investors to re-think asset allocations. Similarly, a reduction in the banks’ balance sheets could also resolve the slope of the yield curve, which is abnormally flat. This results in distortions in discount rates and the way in which firms think about investments.

Disadvantages

As seen in the US in 2013, when there are rumours of QE tapering off, investors holding bonds rapidly withdrew their money from market – known as a Taper Tantrum. Consequently, bond yields drastically increased. This highlights the fact that timing is everything in QE and a move too soon is likely to put pressure on fragile companies and households by driving up rates on mortgages and loans. The IMF are warning that unwinding QE could cause a super taper tantrum increasing volatility in the markets. It is unlikely that a sell off can be avoided when the ‘unwind’ begins.

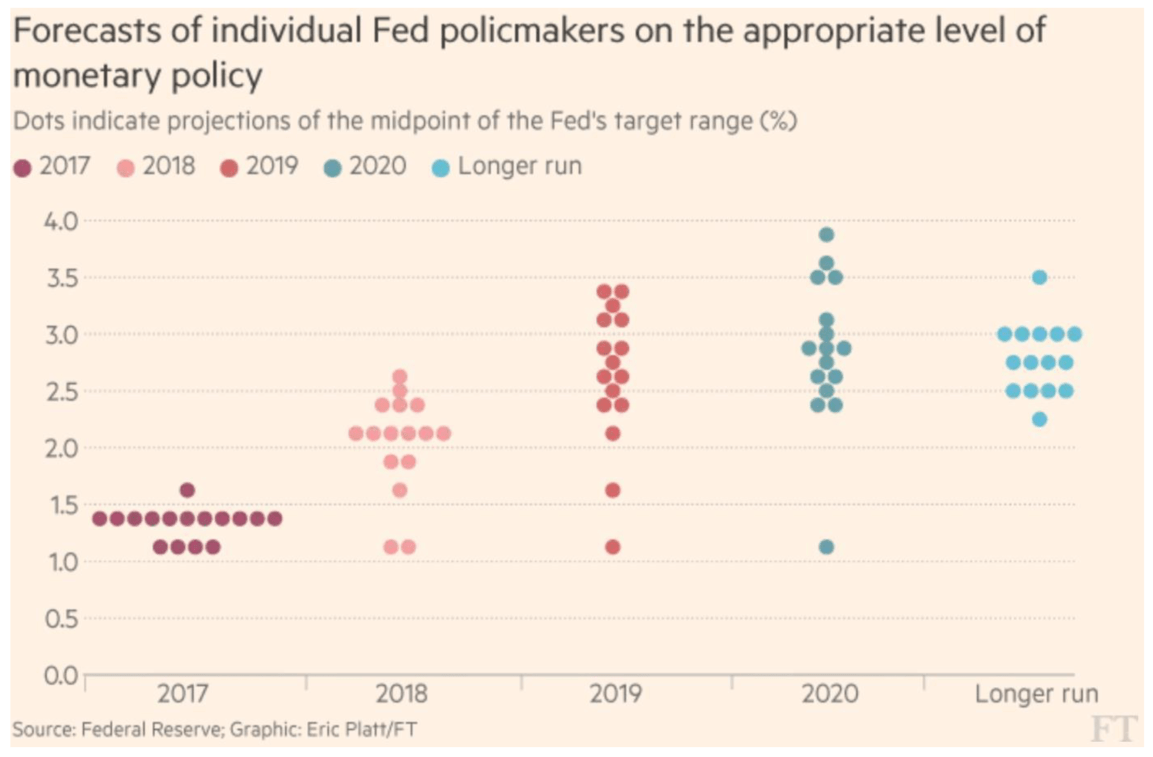

In the US, the Fed have also begun to consider for the long-term potential of the economy as the graph below shows. Without QE, rates are set to rise, which may signal the US economy and the world economy potentially overheating. This forecasted rise will affect duration.

Figure 1: Copyright Financial Times. 2018.

Furthermore, studies have shown that banks have used a large amount of QE to meet their prescribed regulatory buffers. If this money were to be removed, the banks would contest over the remaining liquidity in order to stay within regulations. One way to mitigate against this is to reduce the amount of capital required to be held in buffers. However, this would reduce the banks capabilities to weather a financial storm.

In addition, through repurchasing those securities, central banks have been able to increase the size of their balance sheets, which will encourage other financial institutions to follow along the same path. By increasing the size of their balance sheets, and thus their equity capital, financial institution managers will be able to shield the institution against risks of insolvency as well as meet the necessary requirements for growth under the existing Basel III capital requirements set by regulators. However, whether this increase in size is a benefit to banks remain questionable as banks are known to hold non- performing loans, especially the likes of Italy and Greece due to their respective bailouts.

Additionally, since central banks have purchased roughly £11.3 trillion of financial assets since the crisis, unwinding this could potentially cause another. Reducing the new inflows of money could lead to severe asset decline and liquidity disruptions.

So should QE be done

Quantitative easing was a controversial untested policy in which the central banks had no other quick remedy to prevent a severe depression. The timing of when to unwind QE will play a crucial role in either returning economies to the status quo, or completely upsetting what has been dubbed as the ‘new normal’, leading to further financial pressures. The monetary policy should not defer for short term and temporary economic fluctuations. It should provide a confidence and stability for the economy, in order to guide business and financial decisions. The idea is simply that if unwinding QE has ill-effects, cutting rates remains an option to offset this. Therefore, the monetary policy committee should endeavour to explicitly state its agendas for the future ensuring symmetric information between themselves and the rest of the UK Economy and banking industry.

In summary

Quantitative Easing is suppose to help stimulate the economy but it can be a expensive process in which the benefits it provides can be completely undone when a government tries to halt it. However if they see no other option its crucial to attempt to kick start the economy and help it grow.