- UN votes to impose new North Korea sanctions

- China scraps deposit requirement for trades

- BOE holds rates steady amid high inflation

- US CPI rose 1.9% year on year in August

- US household income rises for second year

- US retail sales disappoint

As tensions continued to escalate between North Korea and the rest of the world, global equities rose slightly. The yield on the US 10-year Treasury note jumped to 2.20% from 2.06% last Friday as the United States began to recover from two major hurricanes. The price of West Texas Intermediate crude oil rose to $49.87 from last Friday’s 47.59 while the Chicago Board Options Exchange Volatility Index (VIX) declined to 10.32 from 12.34.

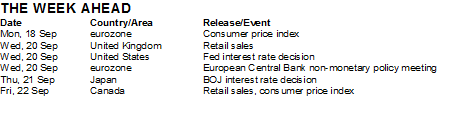

MACRO NEWS

North Korea faces new sanctions

In response to North Korea’s nuclear test conducted a week ago, the United Nations Security Council unanimously voted to adopt the watered-down US draft resolution to impose new sanctions on the country. The resolution is designed to cap the country’s oil imports, ban textile exports, end additional overseas laborer contracts, suppress smuggling efforts and stop joint ventures involving other nations and sanction-designated North Korean government entities. Additionally, China’s five biggest banks froze new accounts of North Korean individuals and companies — an unprecedented effort to suppress financial flows with the country. In response to the resolution, North Korea carried out a ballistic missile test in which it launched for the second time a missile that overflew Japan and landed in the Pacific Ocean. South Korea retaliated for the launch by conducting military drills and its own missile test

Yuan surges, China scales back on measures

The yuan strengthened 6.7% against the US dollar this year, recovering all of last year’s decline of 6.6%. However, the surge is causing a drag on China’s export growth and threatening to deplete profits for many manufacturers selling in foreign markets. In response to this, the People’s Bank of China has removed a deposit requirement for currency forward trades. This will make it less expensive for companies and investors to buy dollars while selling the yuan. In conjunction with this, the central bank removed the reserve requirement on foreign banks’ yuan deposits last week, which will potentially make it easier for foreign investors to bet against the currency. By the end of the month, China is also expected to phase out measures to limit its outbound investment and will instead put in place formal guidelines issued by its State Council in August that encourage foreign deals in areas such as technology.

BOE holds interest rates steady

At Thursday’s monetary policy meeting, the Bank of England voted to keep interest rates at 0.25% but indicated that inflationary pressures may prompt an increase in the coming months. British inflation increased to 2.9% in August, well above the central bank’s target of 2%. The BOE expects inflation to rise to 3% in October before declining. UK unemployment fell to 4.3%, the lowest level in more than 40 years, but wage growth continued to lag behind price increases. Average weekly earnings grew 2.1% over the three-month period, well below inflation.

US consumer prices increased in August

In response to the surge in gasoline and housing rental prices, the US Consumer Price Index jumped 0.4% in August, up from 0.1% in July, and increased 1.9% year on year compared with July’s 1.7%. Gasoline prices increased 6.3% and are expected to rise further in September as a result of the temporary closure of refineries in the wake of Hurricane Harvey.

US household income on the rise

After a long period of stagnant income growth following the 2008 financial crisis, US median household income sustained strong growth for the second consecutive year, rising to 59,039, a 3.2% more than a year earlier, after adjusting for inflation. Income rose across all ages, ethnicities and geographical areas. Simultaneously, poverty levels fell to 12.7%, the lowest level since 2007.

August retail sales miss

Headline August retail sales were down 0.2% month over month, below consensus expectations of a 0.2% rise and worse than July’s downwardly revised 0.3% increase. Core retail sales, which feed into GDP, were down 0.3% month over month, confounding expectations of a 0.3% increase. Auto sales decreased 1.6% month over month, possibly as a result of Hurricane Harvey. Further, sales excluding autos rose just 0.2% compared with an anticipated 0.4% gain. Electronics and appliance stores, building materials and clothing accessories all recorded month-over-month declines. On a brighter note, the Empire manufacturing index for September beat expectations, coming in at 24.4 versus the 18.0 expected. In addition, labor market indicators pointed to a modest increase in employment and hours worked, and both input and selling prices rose at a faster pace than last month.

Repairing damage from US hurricanes expected to cost billions of dollars

In a preliminary analysis, Moody Analytics estimates that damage caused by hurricanes Irma and Harvey could cost between $150 billion and $200 billion to repair, but these figures are expected to change as more information is gathered. The economy could suffer an additional $20 billion to $30 billion in lost economic output from the two storms. As a result, Moody’s expects US GDP to decline a half point to 2.5% for the third quarter but added that it expects fourth-quarter GDP to rally, depending on rebuilding efforts.

Fed expected to announce plan for reducing its balance sheet

At its September policy meeting, the US Federal Reserve will most likely hold interest rates steady at 1.25%. Fed officials are also expected to announce when they will start to reduce the central bank’s $4.5 trillion balance sheet.

Republicans continue to struggle for consensus on tax reform

Despite a barrage of headlines on the subject, the scope and timing of any tax reform remains unclear. At a Politico event on Thursday, US secretary of the treasury Secretary Mnuchin said that a widely anticipated blueprint on taxes due from the “Big Six” group of senators late this month will propose a specific corporate tax rate and discuss in detail the deductibility of corporate interest. He also said reports suggesting that negotiators are far apart are untrue. Reuters reported that Senator Orrin Hatch (R-Utah) said the Big Six will not dictate the direction that the Senate Finance Committee takes on tax reform. Reports noted that some Republicans viewed this comment as one that will widen rifts among Republicans in the Senate, House and White House and could jeopardize reform.

All the best and have a great week

CEO

+60 3 2026 0286