Next year is expected to be another flat and challenging period for the real estate market, with the issue being the lack of affordability which remains unresolved. Although overall consumer sentiment has improved and asking prices have come down, the key issues of affordability overhangs high-rise homes, rising cost of living and tight financing and this will have a dampening effect.

In 2018, properties are expected to remain unaffordable at 4.4 times the median income in Malaysia, with the number expected to be even higher in key urban locations like Kuala Lumpur and Penang. Despite higher gross domestic product (GDP) projected for 2017 and a slight recovery in crude oil prices, the property industry is still hampered by various factors. Higher GDP does not necessarily mean higher wages and disposable incomes for the B40 and M40 segments.

Properties remain out of reach for many Malaysians due to the gap between asking prices in both the primary and secondary markets. B40 refers to the bottom 40% of households with a monthly income of below RM3,900 while the M40 group has household income ranging between RM3,900 and RM8,300. The country’s real estate market is still correcting itself, with a steady downward trend.

It sees possible marginal drops in real estate prices in Kuala Lumpur, Selangor and Penang. The recent bad floods in Penang are expected to have minimal effect on prices in the long term. On improving the supply of affordable homes, one key finding was the possibility of making it compulsory for developers to build affordable homes in their projects, similar to the statutory requirement to allot Bumiputera homes. A gradual improvement in overall consumer sentiment is expected to continue next year.

Similar to the ‘Ripple Effect’ in London there will greater interest in landed suburban properties located some distance from the city centre, particularly those on the outskirts of Selangor. Emerging hotspots, such as Rawang, Shah Alam North, Setia Alam, Ijok, Semenyih and Kota Kemuning, these are expected to continue gaining momentum as the infrastructure improves in the coming years.

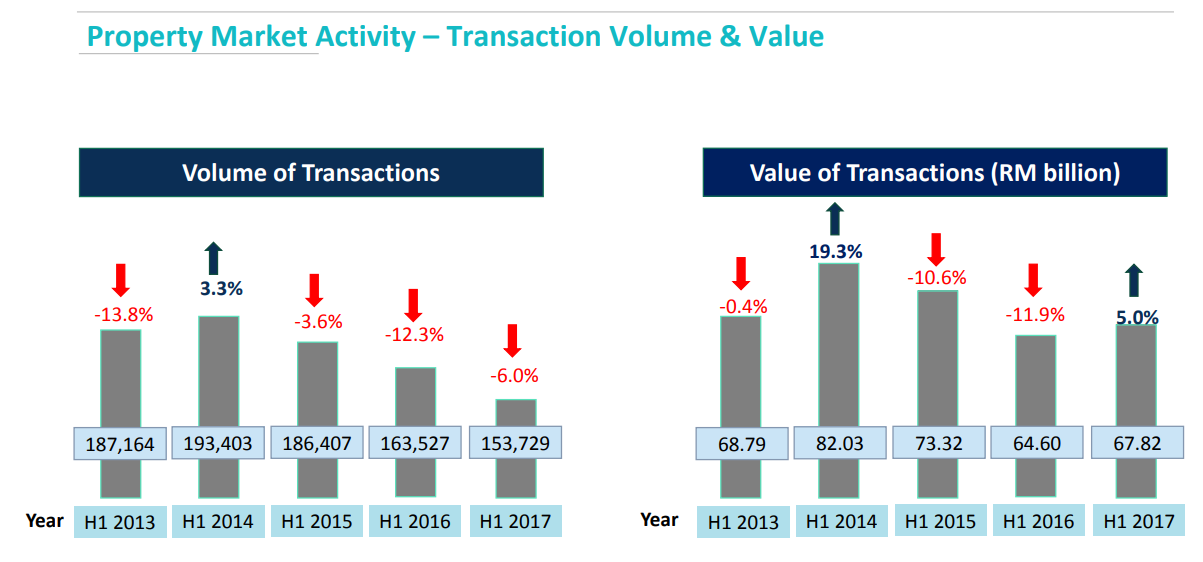

According to Deputy Finance Minister Lee Chee Leong, the number of unsold completed residential units are up 40% to 20,807 units in the first half of 2017 compared with the same period last year. These units are worth RM12.26 billion with condominiums and apartments costing over RM500,000 dominating the unsold homes in Malaysia.

Ernest Cheong, who is a property expert, pointed out that the RM12.26 billion is only from the primary market, which includes launches by developers, it does not include the secondary sale market. With the amount of units unsold it means that developers are in danger of losing their bridging finance from banks as they may fail to hit the sales target because consumers can’t afford to buy the properties. Thus, he predicted that property markets will crash within 24 to 30 months if this situation continues. If the property crash comes early next year, Cheong expects the prices of houses to fall from RM500,000 to RM300,000 and advised Malaysian consumers not to commit to buying a home unless they could save up to RM1,000 a month for at least a year.

In addition, oversupply of property would be exacerbated as there are about 140 malls entering market in key states by 2021. This will potentially become more severe than during the Asian Financial crisis in 1997.

According to the International Monetary Fund, historically housing booms have been followed by busts about 40% of the time, which is associated with longer economic downturns and larger output losses compared to equity market.

Given that there are imbalances in both residential and commercial property segments, Bank Negara in its report, said this is a source of concerns as the property sector has linkages to more than 120 industries, collectively accounting for 10% of Gross Domestic Product and employing 1.4 million Malaysians. Any severe property market imbalances and overbuilding will affect the stability of the financial system.

The central bank had raised this issue to banking institutions and the exposure of the financial institutions on this sector was still at prudent level but property oversupply could impact other sectors. This could pose risk to macroeconomics and financial stability of Malaysia.

The Chinese government has prohibited direct individual investment in overseas property projects, but there are numerous ways to skirt around these restrictions so money coming in from mainland China will still be a positive for Malaysian property but Malaysia cannot just rely on this if they are to be a fully-fledged developed nation.

Malaysia’s population is still growing so demand is still good BUT there is a huge gap between earning capabilities and first time buyers and new families will have to look very carefully over the next few years on whether they can buy instead of renting or living with family.

In long run, I feel Malaysian property prices will stay stagnant and rental income will drop due to the choice and over supply, we have seen high end property slightly decrease in value over the last few years and until the market has more demand will stay relatively flat. Unlike Tokyo, Hong Kong, Singapore, Shanghai, Kuala Lumpur has vast amounts of space to still build properties so comparing the like for like is unrealistic and expectations of large capital growth is not imminent.

Malaysia economic outlook may look more positive if the oil price increases in next few years, this in turn will bring in more expatriate workers, boost rental returns for owners and start creating demand for both local and foreign investors. However, currently there is a little skepticism within the market because of the general election next year which may bring even more changes.

Have a good day

All the best

CEO

+60 3 2026 0286