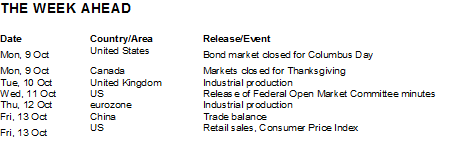

- US retail sales improve, CPI boosted by gasoline

- IMF nudges up global growth forecast

- Brexit talks at apparent impasse

- FOMC on course for December rate hike

Stocks continued their advance into record territory, marking the fifth consecutive weekly gain for the large-cap Dow Jones Industrial Average and S&P 500 Index. The week brought the first releases of major third-quarter earnings reports, with JPMorgan Chase and Citigroup falling Thursday after reporting lower fixed income trading revenues and higher set-asides for credit card losses. Wells Fargo reported an earnings’ decline on Friday, further weighing on the broader financials sector.

Consumer staples stocks performed well, boosted by a surge in Wal-Mart shares after the retail giant announced a massive share repurchase program and predicted a strong rise in online sales. Oil recouped some recent loses, rising to $51.50 per barrel from $49.50 last Friday.

MACRO NEWS

US retail sales rebound in September

After dipping 0.2% in August, US retail sales rebounded strongly in September, rising 1.6%. Higher gas prices in the wake of Hurricane Harvey and a jump in auto sales were major contributors. Higher gas prices also contributed to a 0.5% advance in the Consumer Price Index in September. Stripping out food and energy, prices rose a muted 0.1% last month.

IMF kicks off fall meeting with growth upgrade

As finance ministers and central bankers gather in Washington this week for the fall meetings of the International Monetary Fund (IMF) and World Bank, IMF economists released their latest World Economic Outlook. The fund’s growth forecast was slightly more upbeat, with global gross domestic product expected to expand 3.6% this year and 3.7% in 2018, a 0.1% increase from the last update in July.

IMF chief economist Maurice Obstfeld called the current global acceleration notable because it is more broad-based than at any time since the start of this decade. This year runs counter to many recent years when economists were forced to trim overly optimistic forecasts rather than raise them.

Juncker: Pay first, talk later

European Commission president Jean-Claude Juncker said on Friday that the United Kingdom would need to pay its “divorce bill” before discussions can proceed on trade and future relations between the UK and the European Union.

The EC leader said that negotiations have advanced more slowly than expected and that it is unlikely the European Council will agree when it meets next week that sufficient progress has taken place for negotiations on the future relationship to begin. Earlier in the week EU chief Brexit negotiator Michel Barnier said discussions on the financial settlement were deadlocked.

Fed signals December rate hike likely

Minutes from the September meeting of the US Federal Reserve’s Federal Open Market Committee show that “many” members thought another rate hike was likely to be warranted late this year if the economic outlook remains roughly unchanged.

However, some members expressed concerns that recent soft inflation data may not be temporary, owing to idiosyncratic factors, as the committee has stated in the recent past. Falling prices for things such as mobile phone service and prescription drugs have temporarily suppressed inflation, according to the Fed.

Trump takes executive action on health care

With efforts to repeal and replace the Affordable Care Act blocked in Congress, US president Trump this week issued an executive order to reform the health care sector. The order allows employers to band together to form groups, potentially lowering the cost of coverage. It also allows insurers to offer coverage across state lines.

In addition, the administration is expected to announce later today that it will halt payments to insurers to offset government subsidies for low-income purchasers. Insurance carriers have been raising premiums in recent months in anticipation that the payments would be halted.

ECB setting stage for next policy phase

The European Central Bank appears to be moving towards shifting its exceptionally easy stance over monetary policy before the end of the year. One proposal reportedly being considered by the ECB is to cut in half the rate at which it buys European bonds, from €60 billion to €30 billion beginning in January, and keeping the program active for at least nine months.

At the same time, ECB president Mario Draghi said in Washington that policy rates will not be raised until well past the end of quantitative easing. Markets appear to be focusing on the policy rate forecast more than the QE rumors, with 10-year German bund yields falling 4 basis points on Friday to 0.41%.

European Stocks Rise

European stocks ended the week higher, with two key benchmark indexes, Britain’s FTSE 100 and Germany’s DAX 30, reaching record highs. A slide in the pound boosted investor confidence in the multinational companies that dominate the FTSE 100 and generate sales in foreign currencies. Mining stocks were strong, buoyed by solid import demand from China.

The pan-European benchmark Stoxx 600 ended the week marginally higher. European equity funds posted solid weekly inflows overall, according to EPFR Global data.

All the best and have a great week

Stuart

CEO

Farringdon Group

+60 3 2026 0286

Bitcoin was invented as a peer-to-peer system for online payments that does not require a trusted central authority. Since its inception in 2008, Bitcoin has grown into a technology, a currency, an investment vehicle, and a community of users. In this guide we hope to explain what Bitcoin is and how it works as well as describe how you can use it to improve your life.

Bitcoin was invented as a peer-to-peer system for online payments that does not require a trusted central authority. Since its inception in 2008, Bitcoin has grown into a technology, a currency, an investment vehicle, and a community of users. In this guide we hope to explain what Bitcoin is and how it works as well as describe how you can use it to improve your life.