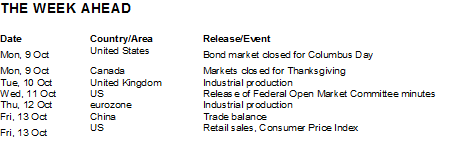

- Nonfarm payrolls fall in wake of hurricanes

- Catalonia expected to declare independence

- Global economy continues to purr

- Fed short list makes rounds

- Trump expected to de-certify Iran nuclear deal

Global equities extended their gains this week, with the MSCI All Country World Index hitting a record high. Solid economic data and hopes for a tax reform package helped push the yield on the US 10-year Treasury note to 2.38% from 2.32% a week ago. West Texas Intermediate crude oil slipped to $49.50 a barrel from $51.50 last Friday while equity volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), closed at a record on Thursday and traded at 9.50 early Friday.

US payrolls fall for first time since September 2010

Hurricanes Harvey and Irma combined to bring an end to a seven-year streak of positive US payroll reports. Thirty-three thousand jobs were lost in September as a result of the storms, though the unemployment rate dipped to 4.2% due to a temporarily smaller labour force. Average hourly earnings rose to an annual rate of 2.9%, but economists warn that storm-related distortions are likely partially responsible for the rise. It is likely to be another month or so before the storms’ impacts work their way through the data. An unexpected positive effect of the hurricanes was a spike in September auto sales as consumers replaced vehicles damaged in the storms.

Declaration of independence expected from Catalonia

Catalonia, the wealthy Spanish region that is home to Barcelona, is expected to declare independence from Spain next week. The move comes in the wake of a crackdown by the Spanish central government on 1 October intended to suppress an independence referendum. Ninety percent of the ballots cast were for independence, with those opposed largely boycotting the vote. Analysts expect next week’s declaration to be largely symbolic, and Catalan leaders are likely to accept a devolution of powers from Madrid, particularly on fiscal matters, rather than pushing for a complete break. Catalonia pays roughly €10 billion more to the Spanish central government than it receives in state services.

Global economy continues expansion

Figures from the United States, Europe and China released this week all showed continued solid economic growth. September figures for the US manufacturing and services sectors both showed their strongest readings in more than a decade, but the US data may have been somewhat distorted by the recent hurricanes. The Institute for Supply Management manufacturing index rose to 60.8, the highest level since September 2004, while the nonmanufacturing reading came in at 59.8, a level not seen since August 2005. European data were similarly robust, and China also showed continued upward momentum.

Trump reportedly narrows the Fed chair field

Bloomberg News reported this week that aides to US president Donald Trump have narrowed the list of candidates for chair of the US Federal Reserve to four, or perhaps five, people. Trump has reportedly spoken with Fed chair Janet Yellen about re-upping, though she is not expected to receive reappointment, according to the report. Sitting Fed governor Jerome Powell, former governor Kevin Warsh and National Economic Council director Gary Cohn have all reportedly spoken with the president about the position, while Stanford University economist John Taylor has apparently not been interviewed but is said to be under consideration. All are known quantities to the markets, with Warsh and Taylor seen as the most hawkish of the group.

Iran nuclear deal expected to be decertified

In a move that will likely draw criticism from European allies, President Trump is expected next week to decertify that the Iran nuclear deal — designed to restrain Iran’s nuclear ambitions — is in the security interests of the US. Presently, the president must certify the agreement every 90 days. If the president withholds certification, Congress then has 60 days to decide whether to reimpose sanctions on Iran. It is possible that the pact will ultimately hold together if Congress does not apply sanctions.

Puerto Rico’s bonds gyrate after talk of restructuring

An offhanded comment from President Trump that the $73-billion debt of Puerto Rico may get wiped out sent the island’s general obligation bonds skidding in price this week. Trading near 44 cents on the dollar before the comments, the bonds fell to around 30 cents before stabilizing, according to the Wall Street Journal. The White House later indicated that it does not intend to get involved in Puerto Rico’s restructuring.

First steps toward US tax reform underway

The US House of Representatives took the first step toward passing a tax overhaul by approving a fiscal- year 2018 budget blueprint. Congress must pass a budget before a tax bill is allowed, under Senate budget reconciliation procedures, to pass in that body with only 51 votes, rather than the 60 needed to end a filibuster. Passage of the House measure ups the odds that tax reform could be enacted early in 2018.

All the best and have a great week

CEO

+60 3 2026 0286