The Final Salary Pension Scheme

The Final Salary Pension Scheme

The black hole in Britain’s final salary pension schemes has grown to a record £390 billion, new data suggests. The deficit of all UK private sector defined benefit schemes has rocketed by £135 billion in the past year alone, the equivalent of a £2.6 billion increase every week, JLT Employee Benefits said. Widening pension deficits are in part triggered by ultra-low interest rates, which drive down the returns on Government bonds held by pension funds

In monetary terms, Royal Dutch Shell has the largest pension deficit. The energy company currently has over £9.5 billion of pension liabilities, equating to a pension deficit of 15%. BT and BP are close behind with £7.5 billion and £7.3 billion of pension liabilities respectively.

BT is appealing to the fund’s trustees and telecoms unions to agree to end accruals in its defined-benefits pension scheme. It has more than 300,000 members and is the UK’s largest private-sector retirement fund.

http://www.telegraph.co.uk/business/2017/05/27/bt-cap-pension-pots-fill-14bn-hole/

In the last 12 months, the total disclosed pension liabilities of the FTSE 100 companies have fallen from £614 billion to £586 billion. Ten years ago, the total disclosed pension liabilities were £407 billion. A total of 16 companies have disclosed pension liabilities of more than £10 billion, the largest of which is Royal Dutch Shell with disclosed pension liabilities of £57 billion. A total of 21 companies have disclosed pension liabilities of less than £100 million, of which 12 companies have no defined benefit pension liabilities.

Situation update

The combined deficit of UK pension funds hit £500 BILLION! To put this in context, it’s the same amount as the GDP of Thailand or South Africa!

Pension experts are predicting that final salary pension schemes could be consigned to the history books, not in decades, but in just three years, as schemes close their doors to new members.

Why?

- Low gilt yield (UK government bond interest)

- Poor performance

- Members not contributing enough

- Higher life expectancy

The Pension Protection Fund (PPF), the government’s private enterprise safety net (not funded or guaranteed by the government) for members of final salary schemes, has stated there are over 5,142 schemes in deficit—representing 81.4% of all UK pension schemes.

The average deficit in funding for clients with UK schemes that I have met is 33%. That’s scary.

What could force a scheme into the PPF?

A firm becoming insolvent or pension fund trustees that just can’t handle the deficit. However, there have been recent cases of firms pushing away their pension fund liabilities.

A recent example of this is when UK Coal went into administration, and their 7,000-member pension pot went into the PPF. This is because the group responsible for repairing the pension deficit, of at least £450mn, sank into a long-anticipated administration.

This means that the guaranteed pension members were expecting will be drastically reduced by up to 50% in some instances.

Some schemes that are on my watch list have huge liabilities:

- BT Group plc, British Airways and BAE Systems plc (the old privatized industry)

- The National Health Service and any Civil Service pension

- The Royal Bank of Scotland plc

- Barclays plc

- Royal Dutch Shell plc

Interest Rates linked to Pension Pot Values

Transfer values are at an all-time high currently, this is due to the post Brexit environment with government bond rates being at an all-time low, as they are correlated with interest rates, meaning employees are getting transfer offers around 30% to 40% higher than they were a few years ago.

Indeed some of these values have increased by as much as 25% in just the last 9 months. Bearing in mind interest rates haven’t been this low in over 200 years, they will soon start to rise, possibly by Q4 this year or the beginning of 2018 meaning the values of Pensions will drop dramatically, add that to a potential reduction in employees benefits in the future by the government, UK Pension schemes will be shockingly bad in the coming years.

https://www.ftadviser.com/pensions/2017/03/08/db-transfer-values-back-to-near-record-highs/

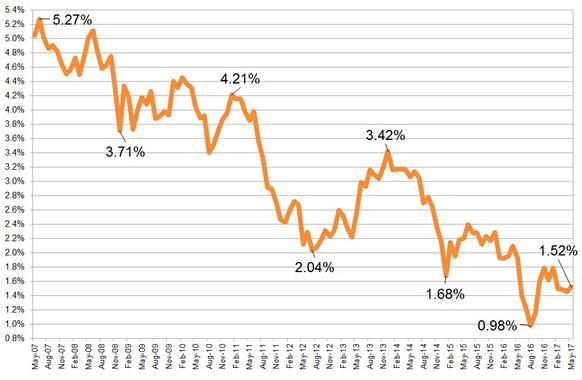

Annuity rates plummet, making 2017 ‘worst year for payouts

2007 = 4.6% – 2014 = 3.2% – 2016 = 2.1% – 2017 = 1.5%

Annuity rates are based primarily on the 15-year gilt yields so changes in gilt yields will affect annuities. The above chart shows yields reached an all-time low of 0.90% on 11 August 2016 after an interest rate cut to 0.25% and £70 billion of quantitative easing. The 15-year gilt yields had reduced significantly since June 2008 due to the financial crisis and this has had the effect of reducing annuity rates.

The drop is the biggest recorded and means over 55s swapping their pension pot for a guaranteed income in retirement today are now faced with some of the worst deals in history as annuity incomes have hit an all-time low.

Data from savings website, Moneyfacts, shows the average standard annuity income for a 65-year-old has fallen by 14.8pc on a £10,000 deal and by 15pc on a £50,000 deal so far during 2016, with potential to fall even further.

Steven Cameron, pension’s director at Aegon, added: “With annuity prices at an all-time low and unlikely to recover soon, people need to start thinking differently and keep their options open. Putting off retirement, continuing to work and save will be an option for some.”

How can they fix the Final Salary Pension problem?

The governments are in talks to allow UK companies to start cutting benefits which is currently being reviewed and will be decided by the winter autumn statement in December 2017. Also remember how harsh they have been in the last year by changing IHT property tax, lowering the LTA (Pension Life time allowance on IHT), putting a 25% tax on moving your pension into a QROPS and changing the Shell offshore Pension scheme to 100% taxable residing in the UK. They are also looking at removing the Pension commencement Lump Sum tax free benefit.

Any future changes the government plans to make, will be unlikely to come with any prior warning allowing you to move your pension and retain the tax benefits.

The problem is so big it is causing economic risk to the whole Pension system and the financial system, the FTSE 100 for example would have to hold back dividends for 1 full trading year, which is not going to happen. Halt trading??

What can you do?

You can move your UK Company Pensions into a Self-Invested Personal Pension (SIPP) is the name given to the type of UK government-approved personal pension scheme, which allows individuals to make their own investment decisions from the full range of investments approved by HM Revenue and Customs (HMRC).

SIPPs are a type of Personal Pension Plan. Another subset of this type of pension is the Stakeholder Pension Plan. SIPPs, in common with personal pension schemes, are tax “wrappers”, allowing tax rebates on contributions in exchange for limits on accessibility. The HMRC rules allow for a greater range of investments to be held than Personal Pension Plans, notably equities and property. Rules for contributions, benefit withdrawal etc. are the same as for other personal pension schemes

Benefits:

- It is a UK Pension Wrapper of your company pensions (You can consolidate all of your pensions under one scheme)

- Much wider selection of investments

- You can hold the pension in multiple currencies

- The internal investments are free of income and capital gains tax

- Take early retirement at 55 rather than 60/65 with Final Salary

- 25% tax free lump sum at 55% depending where you are residing

- On the event of your death your wife/family will get 100% of the remaining pension fund, (Final Salary Scheme – You will only receive 50%/60%, then should anything happen to your wife the children will get 0) with a SIPP they will get 100% of the remaining pot, allowing for greater inheritance benefits.

If you have a frozen defined benefit (DB) pension plan or final salary scheme, there has never been a better time to transfer into a SIPP Self Invested Personal Pension. WHY?

Transfer values are 80% higher today than they were six years ago, due to post Brexit and extremely low interest rates, which will not last long possibly by the end of 2017

Sit down and review your current situation, including the pension itself and the scheme. We have seen an increase in individuals who are fearful of the current UK pension crisis—with good reason.

However, there is an unprecedented window of opportunity available to eligible DB scheme members today, that may not be there by the end of this year.

Due to the complex and convoluted nature of pensions and pension transfers, we have an established a specialist pensions division and commissioned independent actuaries to review and report on the status of pension schemes for interested individuals.

This is a simple step to initiate, with no obligation to act on the results of the review. In many cases this action has already preserved and protected significant transfer amounts, converting a future promise into a real investment today for the benefit of the scheme member, spouse, children, and children’s children.

If you would like a valuation on your pension please contact me directly on +60 3 2026 0286 or email to stuart@farringdongroup.com and we will uncomplicate this information and inform you of the options.

Thanks and have a great day

CEO

Kuala Lumpur : Malaysia

If you feel that this is of interest to colleagues, friends or family, please feel free to forward this information on.