Love or hate stories that are negative about the currency that you use on a daily basis, it is something we all need to understand and more importantly plan for!

I held a seminar two weeks ago and I was surprised with how many people agreed that Malaysia’s currency is not going to recover quickly. The room was filled with Malaysian citizens and from my previous seminar experiences, Malaysian’s will normally fight for the positives and why their currency will recover and things will be Ok……. but this time, something was different, it was obvious that concern for livelihood outweighed any hope for their government to right the freefalling currency.

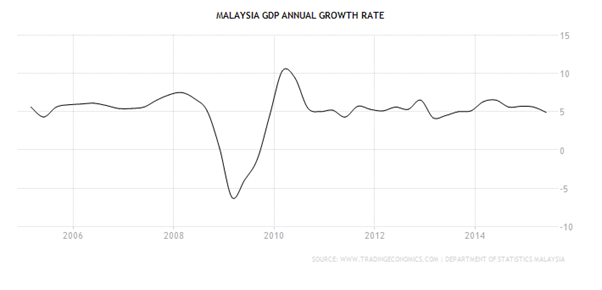

The first thing to look at is Malaysia’s growth…..or should I say Putrajaya’s quote of 4.5% – 5.5%. This to me is a bold statement and with the current political issues, economic issues, I find this hard to believe. One issue to begin with is the way Asia and the West state their figures in the first place.

In the West, it’s common for predictions to be put out there and then often revised up. This is most likely to give that positive news that they beat predictions and confidence grows. Whereas in the East it is the other way around, figures are stated and then often revised down. I for one fear a prediction of 4.5% – 5.5% is a little too confident and I would like to explain why with facts and figures.

“According to S&P, Malaysia has the highest personal debt among 14 Asian economies, with the rate jumping to 88 percent of gross domestic product from around 60 percent in 2008.” 07/09/2015

In addition to this, Moody’s uprated Malaysia rating to a neutral outlook in June, however were in KL as little as three weeks ago to reconsider this and I fear with the current climate, Malaysia will be put back to A- negative outlook.

Here are a few facts that I have pulled from media recently.

- Malaysia’s manufacturing sector recorded a sharp decline in activity in August, with new orders contracting at the fastest rate since September 2012

- The headline Purchasing Managers Index (PMI) dropped to 47.2 ― down from 47.7 in July ― which the index rated as the “strongest deterioration in operating conditions” for Malaysian manufacturers in nearly three years

- New orders at Malaysian goods producers contracted for the sixth month in a row

- Moreover, the rate of decline was the second-sharpest in the series history

- Job hiring have posted a 26 per cent decline this year

- The Malaysian equity index fell 15 per cent from its July 2014 high

- The MYR currency is Asia’s worst performer this year as political uncertainty clouded the outlook amid an emerging-market selloff

Now let me cover a couple of MAJOR factors as to why Malaysia’s RM will not recover quickly and the economic outlook is poor.

Putrajaya have played down the importance of Oil and said that Malaysia has many other factors that will assist in good GDP figures in 2015.

Before I disprove Putrajaya’s poor comments, let me start with Oil.

In 2014 oil revenue were 31% of Malaysia’s GDP and for 2015 this is expected to fall to 22% based on oil at USD55.

Oil has faltered this year and gone down as far as USD38. This in itself should mean that even a 22% prediction will most likely be in the teens.

Many pro government writers begin telling you that we should not worry, our economy is based on so much more…….so what are they?

- Tourism: Q1 stats show 600,000 less visitors and this expected to be worse in Q2, not to mention the world media damaging Malaysia as a peaceful country. This will of course cause holiday makers to reconsider coming to Malaysia for a holiday, despite a weak currency. What family would risk their children’s safety when all they see is multiple rallies, murders, corruption! Whether these stories are true or false, it paints Malaysia in a very bad light and I believe tourism figures to be very bad in Q3 and Q4.

- Natural Gas : Prices have been down and very low for a decade and I will not dwell too long on proving this, you can have a google and see this for yourself

- Banking & Services: Scandals and a falling RM, destroy confidence in the markets. Whether stories are true or not, people simply do not trust the Malaysian banking sector at the moment and large amounts of deposits are leaving the country

- Palm Oil : Production is drastically down since December 2014 where it dropped 11% and figures do not seem to be recovering

I do not for see the RM bouncing back anytime soon and I fear that even with the government’s new stimulus package this will simply flat line it at current levels for a few weeks/months. Ultimately, Asia is in crisis, with the RM being the bottom of the pile.

Predictions:

- Numerous rating agencies will initially say that Malaysia is being watched stringently and most likely they will be put on a negative rating or even worse drop the A- lower. (Fitch: Recently moved this up to A- with a neutral standing)

- International perception of Malaysian markets will go from bad to worse, because bad news sells!

- Banks will become less willing to lend and debt collection will be paramount. Mr Chaucer on BFM in September clearly shows that lending and banking deposits are close to 1 : 1. This means that lending is now drying up and house and car loans are already decreasing

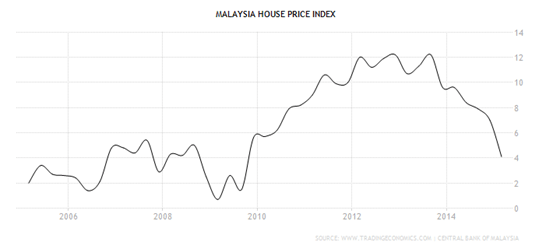

- The knock on effect of this is the housing market, which I have said in previous stories that it is way overpriced and you can see on the graph below that transactions have gone to a third of where they previously were. Event those property agents that always tell us everything is fine can have a dose of reality now that they see that housing is the next thing to go down.

- These low house sales, drying up of lending and negative equity will result in home owners owing more than their homes are worth and repossessions will rise. I witnessed this in the UK market crash and Malaysia has a lot of similar alarm bells ringing. Even those people that think landed property will be fine………I will prove myself right in the coming quarters. Malaysia’s house prices whether in apartments or landed, will fall and I can’t see them coming back quickly. People are renting houses at less than 2% rental yield……..my house is 1.8% for my landlord, so I can see this with my own situation.

- This will be the same with car loans & those people who can’t even afford a 1 bedroom apartment but drive a brand new Porsche Cayenne on finance will also start to worry!

- The housing market correction, bad economic data, job losses increasing, oil prices staying down and corruption issues will take a minimum of 2 – 3 years to put right and the low RM rate is here to stay for some time.

I consider Malaysia my home and I see that it has so much potential, but at the moment, economically, politically and perception is not great. The best thing for people to do is speak to a professional about how to limit their exposure to these issues and maybe consider investing away from Malaysia. I for one, certainly think that anyone holding too much RM will be best advised to move it to a strengthening currency.

Thanks for reading

Stuart Yeomans

Farringdon Group CEO